Here's the thing: federal tax incentives can dramatically change that math. When you combine the Investment Tax Credit (ITC) with accelerated depreciation, many businesses recover well over half their installation cost through tax benefits alone — often in year one.

This guide covers the two core federal tax benefits for business solar, how ITC bonus adders can push credits above 40%, what the One Big Beautiful Bill changed about deadlines and depreciation, and what California-specific incentives apply to Southern California businesses.

Key Takeaways

- The federal ITC provides a dollar-for-dollar tax credit of up to 30% of your solar installation cost

- MACRS accelerated depreciation adds further deductions — and 100% bonus depreciation is back for qualifying installations

- Combined, these benefits can offset 60%+ of upfront costs in year one

- The One Big Beautiful Bill requires most businesses to begin construction before July 5, 2026 to lock in eligibility

- California stacks SGIP rebates, a property tax exclusion, and net metering on top of federal benefits

The Two Main Tax Benefits for Businesses Installing Solar

The federal government offers two distinct financial rewards for businesses that install solar: the Investment Tax Credit and accelerated depreciation under MACRS. Using both together produces the strongest financial outcome — they're not mutually exclusive.

Credit vs. Deduction: Why It Matters

A tax deduction reduces your taxable income. If you're in the 37% bracket and claim a $30,000 deduction, you save $11,100 in taxes.

A tax credit reduces your actual tax bill. A $30,000 credit means $30,000 directly off what you owe — regardless of your tax bracket.

For a $100,000 solar system with a 30% ITC, that's $30,000 straight off your federal tax bill. Not a deduction. Not a reduction in income. Off the bill itself.

Who Qualifies

Both benefits are available to most business structures:

- Sole proprietors

- LLCs (taxed as partnerships or corporations)

- S-corps

- C-corps

Your business must own the solar system outright. If you lease panels or sign a power purchase agreement (PPA), the leasing company claims the credits, not your business. Purchase or a loan qualifies; leasing does not.

Tax-exempt organizations have a separate path: the Inflation Reduction Act created a direct-pay option under Section 48 that allows qualifying tax-exempt and governmental entities to receive the credit as a tax payment rather than an offset.

The Federal Solar Investment Tax Credit (ITC): What Businesses Need to Know

The ITC is codified under Section 48 of the U.S. tax code. It provides a direct, dollar-for-dollar federal tax credit based on the total installed cost of the solar system — equipment and labor both count.

The 30% Rate and How to Qualify

The base ITC rate is 6%, but it increases to 30% when one of the following conditions is met:

- The project meets prevailing wage and apprenticeship (PWA) requirements

- The system output is under 1 MW

- Construction began before January 29, 2023

Most small and mid-sized commercial installations under 1 MW qualify for the full 30% without needing to navigate PWA rules. For larger projects, confirm PWA compliance with your contractor and tax advisor before assuming the 30% rate applies.

Carry-Back and Carry-Forward

If your business doesn't owe enough tax in the year the system goes live, the ITC doesn't disappear. Per IRS Form 3800 instructions, unused credits can be:

- Carried back 3 years (applied against prior tax liability)

- Carried forward 20 years (applied against future tax liability)

Businesses with recent losses or uneven income cycles can still capture the full credit value — just across a longer time horizon.

Recapture Rules

If you sell the system, it's destroyed, or it stops being used for a qualifying business purpose within five years of being placed in service, the IRS may recapture a portion of the credit. Per Form 4255 instructions, the recapture schedule is:

| Years in Service | Recapture Percentage |

|---|---|

| Less than 1 year | 100% |

| 1 year | 80% |

| 2 years | 60% |

| 3 years | 40% |

| 4 years | 20% |

| 5+ years | 0% |

How to Claim It

Businesses claim the ITC by filing IRS Form 3468 with their annual tax return. Consult a CPA before installation. The following documentation needs to be in place from day one — not assembled retroactively:

- Purchase invoices for equipment and labor

- In-service date records confirming when the system went live

- Proof of adder eligibility (PWA compliance, domestic content, etc.)

Starting the paperwork early prevents disqualification during an audit.

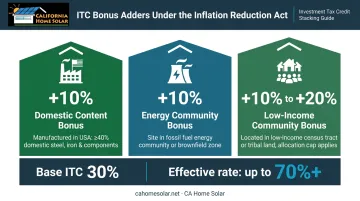

ITC Adders: How Businesses Can Earn More Than 30% Back

The Inflation Reduction Act introduced "adders": bonus credits that stack on top of the base 30% ITC for commercial projects meeting specific criteria (not available for residential solar under Section 25D).

The Three Main Adders

| Adder | Bonus | Key Requirement |

|---|---|---|

| Domestic Content | +10% (with PWA) | At least 40% of manufactured components are U.S.-produced |

| Energy Community | +10% (with PWA) | Project located in a brownfield site or area with fossil fuel industry decline and qualifying unemployment |

| Low-Income Community | +10% to +20% | Facility under 5 MW AC in a qualifying low-income community or on Indian land; requires IRS capacity allocation |

These adders are stackable. A project qualifying for all three could push the effective credit rate above 40% of total system cost.

On domestic content: California Home Solar sources American-made solar panels, which supports clients working toward that qualification. Keep in mind the full calculation covers inverters, racking, and other manufactured components, so confirm the complete supply chain with your installer and tax advisor to verify the threshold is met.

Adder eligibility has to be built into the project design from the start. Discuss it with your solar contractor early in the planning process, not after permits are pulled.

MACRS Accelerated Depreciation for Commercial Solar

Beyond the ITC, businesses can separately claim depreciation deductions on the solar system — reducing taxable income further through MACRS (Modified Accelerated Cost Recovery System).

Calculating Your Depreciable Basis

When you claim the ITC, the IRS requires a basis reduction: the depreciable amount is reduced by 50% of the credit taken.

For a $100,000 system with a 30% ITC:

- ITC claimed: $30,000

- Basis reduction: $15,000 (50% of the credit)

- Depreciable basis: $85,000

That $85,000 is what you depreciate — not the full $100,000.

100% Bonus Depreciation Is Back

The One Big Beautiful Bill (Public Law 119-21, enacted July 4, 2025) reinstated 100% bonus depreciation for certain qualified property acquired and placed in service on or after January 19, 2025. Qualifying installations can deduct the full $85,000 depreciable basis in year one.

One significant caveat applies, however. The OBBBA also removed solar and wind energy property from the standard 5-year MACRS classification for property beginning construction after December 31, 2024. Confirm these details with your CPA before filing:

- Which construction start date governs your project

- Whether your asset qualifies under Section 48, 48E, or another category

- The applicable depreciation schedule based on your specific situation

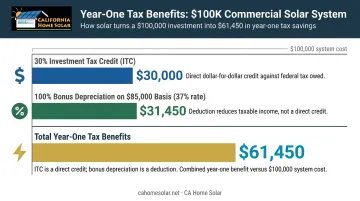

The Combined Savings: A Real Example

Using the DOE's business solar example as a reference, here's the full year-one tax picture for a $100,000 system at a 37% individual tax rate:

| Benefit | Calculation | Tax Savings |

|---|---|---|

| 30% ITC | Direct credit | $30,000 |

| 100% bonus depreciation on $85,000 basis | $85,000 × 37% | $31,450 |

| Total year-one tax benefit | $61,450 |

That's $61,450 back in year one on a $100,000 system — and that's before electricity savings or California-specific incentives reduce your net cost further. For commercial property owners in Southern California, those state-level programs can push the effective payback period down considerably.

Important Deadlines and the One Big Beautiful Bill

The One Big Beautiful Bill (P.L. 119-21) changed the timeline for claiming solar tax credits. Miss the key dates below and your project may not qualify — so plan your installation timeline before committing to equipment or financing.

The Core Deadline

Under the OBBBA, the Section 48E credit terminates for solar facilities placed in service after December 31, 2027, if construction begins after July 4, 2026. Projects that begin construction before that date and meet continuity requirements can still qualify.

Two Paths to Lock In Eligibility

Path 1: Begin construction by July 5, 2026 Start physical construction before the cutoff. If you do, the continuity safe harbor allows you until December 31, 2030 to complete and place the system in service.

Path 2 : Full installation by December 31, 2027: Have the system fully installed and operational by this date regardless of when construction started, subject to the July 4, 2026 construction-start requirement.

IRS Notice 2025-42 clarifies that the traditional 5% spend safe harbor is generally not available for most commercial solar projects under the OBBBA. The exception: systems with a maximum net output of 1.5 MW AC or less (low-output facilities) can still use either the physical work test or the 5% safe harbor. Larger projects must rely on the physical work test only.

FEOC Requirements Starting in 2026

For projects beginning construction in 2026, at least 40% of manufactured components must come from non-prohibited foreign entity sources. IRS Notice 2026-15 provides interim guidance, with more detailed regulations expected. The IRS has not yet finalized the restricted country list, so discuss sourcing compliance with your installer before committing to equipment.

California-Specific Solar Incentives for Business Owners

Federal incentives apply nationwide, but California layers additional benefits on top. For Southern California businesses, three programs are most relevant.

Self-Generation Incentive Program (SGIP)

SGIP provides rebates for battery storage systems paired with solar. Current step rates for commercial storage vary by project type and utility territory — Large-Scale Storage Step 5 rates and equity-based rates are tracked at SGIP Program Metrics, which updates as funding steps are exhausted.

SGIP administrators include SCE, PG&E, SoCalGas, and LADWP. Incentive rates differ by administrator, and LADWP commercial clients have separate programs from IOU customers.

Property Tax Exclusion

California's Revenue and Taxation Code Section 73 provides that installing a qualifying active solar energy system will not trigger a property tax reassessment on your existing property. The California BOE confirms this exclusion protects the added value of a solar installation from increasing your property tax bill — and unlike SGIP, it carries no funding caps or application competition.

Net Metering (Net Billing Tariff)

California's current Net Billing Tariff uses avoided-cost values for exported electricity — generally lower than import rates. For commercial properties under SCE, PG&E, or SDG&E, the ROI calculation for solar now depends more heavily on self-consumption than it did under NEM 2.0. LADWP customers operate under a separate commercial solar structure, including a Feed-in Tariff option for eligible projects.

Navigating these utility-specific structures — different administrators, tariff types, and service territories — is where local expertise pays off. California Home Solar, a Top 500 Solar Contractor with 36 years serving Los Angeles and Southern California, can identify which incentives apply to your property, utility territory, and system design.

Frequently Asked Questions

What is the IRS solar tax credit for businesses?

The IRS business solar tax credit — the Investment Tax Credit under Section 48 — is a dollar-for-dollar federal credit equal to up to 30% of total solar installation costs. It's claimed using IRS Form 3468 and directly reduces your tax bill, not just your taxable income.

What are the tax credits for businesses in 2026 for solar panels?

In 2026, businesses can claim the full 30% federal ITC plus adders up to +10% each for domestic content, energy communities, and low-income areas. To lock in eligibility, construction must start before July 5, 2026 — and qualifying installations may also benefit from 100% federal bonus depreciation.

Can I claim the solar tax credit if my business leases the solar panels?

No. The ITC and MACRS depreciation only apply to the system owner. If your business leases solar panels, the leasing company claims the credits — not you. Business owners must purchase or finance the system to benefit.

How do I claim the federal solar tax credit on my business taxes?

File IRS Form 3468 with your annual tax return. Work with a CPA before installation to confirm documentation is ready: purchase invoices, proof of in-service date, and any adder eligibility records.

What is MACRS depreciation and how does it apply to commercial solar?

MACRS lets businesses recover solar equipment costs through depreciation deductions. With 100% bonus depreciation available for qualifying installations, you can deduct the full depreciable basis — 85% of system cost when the 30% ITC is claimed — in year one. Treatment varies by construction start date, so confirm the details with your CPA.

Does California offer additional solar incentives for businesses beyond the federal credit?

Yes. California offers SGIP rebates for paired battery storage, a property tax exclusion under Revenue and Taxation Code Section 73, and net billing export compensation. Local utility rebates may also apply depending on whether your property is served by SCE, LADWP, or another utility.