Commercial solar has moved well beyond being an environmental statement. With the right incentive stack, it's one of the strongest capital investments available to Los Angeles-area business owners right now.

This guide breaks down every major federal and California-specific commercial solar incentive—tax credits, depreciation, grants, loans, and utility programs—and explains how to combine them for maximum financial impact.

There's also a deadline you need to know: commercial construction must begin by July 4, 2026 to qualify for the federal Investment Tax Credit. That window is narrower than most business owners realize.

TLDR: Key Commercial Solar Incentives at a Glance

- Federal ITC: 30% dollar-for-dollar tax credit on total installed system cost (when prevailing wage requirements are met); construction must begin by July 4, 2026

- MACRS + Bonus Depreciation: Solar property placed in service after Jan. 19, 2025 may qualify for 100% first-year bonus depreciation (under the One Big Beautiful Budget Act)

- USDA REAP Grants: Rural businesses and agricultural producers can receive grants covering up to 50% of project cost, up to $1,000,000

- PACE Financing: Repay through your property tax bill with no upfront capital required

- California adds SGIP storage incentives (up to $1,000/kWh), NEM Net Billing credits, and utility demand response programs — all stackable on top of federal benefits

Why 2026 Is a Pivotal Year for Commercial Solar Investment

The federal solar incentive landscape shifted when the One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025 as Public Law 119-21. It created hard construction and placed-in-service deadlines that businesses cannot retroactively avoid.

The broader market is moving fast. According to SEIA's 2025 Year in Review, the U.S. commercial solar segment added 2,345 MWdc in 2025, with notable highlights:

- 6% year-over-year national growth

- California captured 39% of all commercial installations nationally

- California posted 28% year-over-year growth — driven heavily by SCE and LADWP service territories

Those numbers reflect decisions being made right now, before the OBBBA deadlines close the window on the most valuable incentive stacking. For Southern California businesses, the underlying economics are compelling on their own.

The Business Case Beyond Incentives

Even before incentives, commercial solar addresses four concrete business problems:

- Operating cost reduction — displace expensive grid electricity with owned generation

- Rate hedge — lock in predictable energy costs as SCE and LADWP rates continue climbing

- Property value — income-producing solar assets increase assessed and market value

- Sustainability positioning — required by many corporate tenants and ESG reporting frameworks

The incentives compress the payback timeline. Miss the 2026 deadlines, and projects that pencil out in 4 years may take 7 instead.

The Federal Investment Tax Credit (ITC): The Cornerstone Incentive

The ITC is a dollar-for-dollar reduction in federal tax liability. Under Section 48E, the base credit rate is 6%, increased to 30% when prevailing wage and apprenticeship (PWA) requirements are met. For commercial systems under 1 MW AC, the PWA requirement is excepted—meaning smaller systems can access the 30% rate without the compliance burden.

The credit covers:

- Panels, inverters, and racking

- Wiring and balance-of-system components

- Installation labor

On a $500,000 system, that's $150,000 directly off your federal tax bill.

The Construction Deadline

Per IRS Notice 2025-42, the Section 48E credit terminates for facilities placed in service after December 31, 2027 if construction begins after July 4, 2026. Miss that start date and the credit is gone—there's no partial credit for applicable wind and solar facilities.

Two methods prove construction has begun:

- Physical Work of Significant Nature — meaningful onsite construction activity has commenced

- Five Percent Safe Harbor — for systems with maximum net output of 1.5 MW AC or less, paying or incurring at least 5% of total project cost locks in eligibility

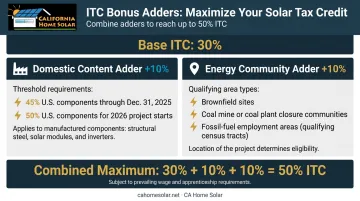

Bonus Credit Adders

Beyond the base 30%, two adders can push up the total credit:

| Adder | Amount (with PWA) | Eligibility |

|---|---|---|

| Domestic Content | +10% | U.S.-manufactured component threshold: 45% for construction through Dec. 31, 2025; 50% for 2026 starts |

| Energy Community | +10% | Brownfields, coal-closure areas, or statistical areas with ≥0.17% fossil-fuel employment |

A project hitting both adders reaches a 50% total credit—half the project cost returned as tax savings.

Equipment selection also affects eligibility beyond domestic content thresholds. FEOC (Foreign Entity of Concern) rules take effect January 1, 2026—facilities whose construction begins after 2025 may lose ITC eligibility if they include material assistance from prohibited foreign entities. The IRS hasn't issued final guidance yet, so equipment specifications made today could need revisiting before breaking ground. Confirm panel and inverter sourcing with your installer before locking in a procurement plan.

Depreciation Benefits: MACRS and Bonus Depreciation

Tax credits reduce what you owe. Depreciation reduces what you earn—your taxable income. Used together, they create a front-loaded financial return that can offset a substantial share of project cost in year one.

MACRS: The 5-Year Schedule

Commercial solar equipment has traditionally qualified for a 5-year MACRS depreciation schedule. Important caveat from IRS Publication 946 (2025): solar or wind property beginning construction after December 31, 2024 is no longer 5-year property under the prior solar/wind rule due to P.L. 119-21. Confirm current MACRS classification with your tax advisor for projects starting in 2025–2026.

ITC Basis Reduction

When you claim the ITC, the IRS reduces your depreciable basis by 50% of the credit amount. With a 30% ITC, your depreciable basis becomes 85% of total project cost.

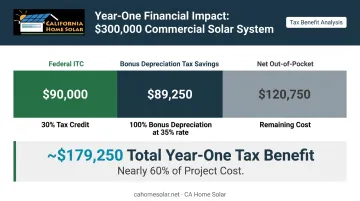

Example ($300,000 system):

- ITC: 30% × $300,000 = $90,000 tax credit

- Depreciable basis: $300,000 − ($90,000 × 50%) = $255,000

Bonus Depreciation: The OBBBA Change

The OBBBA restores 100% first-year bonus depreciation for eligible property acquired and placed in service after January 19, 2025. This supersedes the TCJA phase-down schedule (40% in 2025, 20% in 2026), making the timing of placement-in-service critical.

Combined year-one impact on that $300,000 system:

- $90,000 ITC (dollar-for-dollar tax reduction)

- Plus 100% bonus depreciation on $255,000 depreciable basis — at a 35% effective tax rate, that's roughly $89,250 in tax savings

- Total year-one tax benefit: approximately $179,250 — nearly 60% of the project cost

The ITC, basis reduction, and bonus depreciation interact in ways that vary by tax situation — work with a CPA experienced in energy tax incentives to run the numbers for your project.

Commercial Solar Grants and Loan Programs

USDA Rural Energy for America Program (REAP)

REAP is the primary federal grant program for commercial solar outside of the tax credit system. It provides grants covering up to 50% of eligible project costs, with a maximum grant of $1,000,000 for renewable energy systems.

Eligibility requirements:

- Rural small businesses must be located in areas with populations of 50,000 or fewer and meet SBA size standards

- Agricultural producers must derive at least 50% of gross income from farming operations

- Combined grant and guaranteed loan funding can cover up to 75% of total eligible project costs

Important 2026 note: As of March 31, 2026, USDA was not accepting new FY2026 REAP applications for renewable energy systems under the October 2024 notice. Check the USDA REAP program page for current application windows before committing to this funding source.

REAP grants can be stacked with the federal ITC and depreciation benefits—for eligible rural businesses, this combination can cover the majority of project cost.

Financing Options

Grants aren't the only path. These financing structures can reduce or eliminate upfront costs for businesses that don't qualify for REAP or want to layer in additional funding.

PACE (Property Assessed Clean Energy)

Businesses repay the loan through their property tax bill over time—no upfront capital required. LA County's PACE program explicitly supports onsite power generation projects, and active California C-PACE programs include CSCDA Open PACE and CaliforniaFIRST/Renew Financial.

California Home Solar is a HERO Registered Contractor with experience in PACE programs including California First and Ygrene. Contact their team to confirm current commercial availability for your specific project.

DOE Loan Guarantee Program (Title 17)

The federal government backs commercial clean energy loans through private lenders, with guarantees up to 90% of the debt. This program targets large-scale projects in the $100M+ range and works best for major commercial or industrial developments.

Power Purchase Agreements (PPAs)

For businesses that don't want to own the system, a PPA provides solar electricity at a contracted rate—often below current utility rates—with no upfront cost. Structured correctly, a PPA can be cash-flow neutral or better from the first month. The trade-off: you don't capture the ITC or depreciation benefits directly.

California-Specific Commercial Solar Incentives

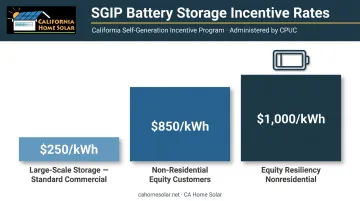

SGIP: Battery Storage Incentives

The Self-Generation Incentive Program (SGIP), administered by the CPUC, provides financial incentives for on-site energy storage paired with commercial solar. Current incentive rates include:

- $250/kWh for Large-Scale Storage (standard commercial)

- $850/kWh for Non-Residential Equity customers

- $1,000/kWh for qualifying Equity Resiliency nonresidential customers

For LA-area businesses facing SCE or LADWP demand charges, battery storage paired with solar is one of the most effective bill reduction strategies available. California Home Solar has helped Los Angeles commercial clients identify and pursue SGIP incentives alongside solar installations. Call 877-903-1012 to discuss how these rates apply to your project.

NEM 3.0 / Net Billing Tariff

New commercial interconnection applications filed after April 15, 2023 take service under California's Net Billing Tariff (NBT) rather than legacy NEM. The NBT provides a 9-year legacy period for the original customer and credits exported electricity, though at rates that differ from the legacy structure.

The practical implication is that battery storage has become far more important for commercial solar economics under NBT. Key design priorities include:

- Maximize self-consumption rather than exporting excess generation

- Use storage to shift energy use into lower-rate periods

- Size systems based on on-site load, not export potential

Sales Tax and Utility Programs

Beyond net billing, California offers additional incentive layers worth evaluating. The partial sales tax exemption (currently 5%) applies to solar equipment in qualifying agricultural applications. Standard commercial installations don't automatically qualify; eligibility depends on purchaser status and primary use.

Utility demand response programs add another layer of savings:

- SCE Emergency Load Reduction Program: $2/kWh for reducing energy use during demand events

- LADWP Demand Response: $0.25/kWh reduced during events

Neither utility has verified direct commercial solar rebates in current official materials. Check SCE's business savings page and LADWP's commercial programs portal for current offerings.

How to Stack Incentives for Maximum Commercial Solar ROI

A Southern California commercial property owner can realistically combine:

- 30% federal ITC (dollar-for-dollar tax credit)

- 100% bonus depreciation on the adjusted basis (under post-OBBBA rules)

- SGIP storage incentives (up to $1,000/kWh for qualifying storage capacity)

- Net Billing Tariff credits for exported or banked generation

- Demand response program payments from SCE or LADWP

On a $500,000 commercial installation, year-one tax benefits alone — ITC plus bonus depreciation — can offset $200,000 or more of project cost, with utility bill reductions continuing to compound across the system's 25+ year life.

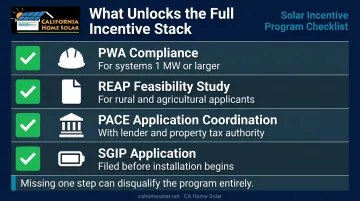

What Unlocks the Full Stack

Qualifying for each incentive requires separate documentation and compliance steps:

- PWA compliance for systems 1 MW or larger (required for full 30% ITC)

- REAP feasibility studies for rural/agricultural applicants

- PACE application coordination with your lender and property tax authority

- SGIP application filed through your utility before installation

Each program has its own filing deadlines, eligibility criteria, and documentation requirements. Missing a single step — like filing the SGIP application after installation begins — can disqualify you from that program entirely. An experienced, licensed commercial solar contractor who knows both the technical and compliance sides keeps the full incentive stack intact.

Getting Started: The Clock Is Running

With the July 4, 2026 ITC construction deadline, the timeline for a commercial project initiated today is tighter than most business owners expect. Permitting, engineering, and utility interconnection approvals take time—often 3–6 months before a shovel breaks ground.

California Home Solar works with commercial clients across Los Angeles County and Southern California through a structured process:

- Facility assessment and financial analysis — including full incentive stack review

- System design and permitting — coordinated with utility interconnection

- Installation and meter commissioning — with compliance documentation handled throughout

To get a complete incentive analysis before construction begins, contact their team at 877-903-1012 or info@cahomesolar.com.

Frequently Asked Questions

Can you put solar panels on a commercial building?

Yes. Offices, warehouses, retail centers, and industrial properties can all install solar—on rooftops or as carport structures. Installation requires a roof condition assessment, structural evaluation, and local permitting. Any qualified commercial solar contractor handles these steps as part of a standard project scope.

What is the commercial solar tax credit for 2026?

Businesses that begin construction by July 4, 2026 can claim the federal Section 48E ITC at 30% of total installed system cost (with prevailing wage compliance, or for systems under 1 MW AC). Domestic Content and Energy Community bonus adders can push the total credit to 40–50%.

Can commercial solar grants and tax credits be combined?

In most cases, yes. USDA REAP grants can be stacked with the federal ITC and depreciation benefits, though the grant amount may reduce the depreciable basis. A tax professional with energy credit experience should review the specific project structure before finalizing the financing plan.

How does MACRS depreciation work for commercial solar?

MACRS allows businesses to depreciate commercial solar equipment on an accelerated schedule rather than over 20+ years. Under post-OBBBA rules, eligible solar property placed in service after January 19, 2025 may qualify for 100% first-year bonus depreciation, with the depreciable basis reduced by 50% of any ITC claimed.

How long does it take for commercial solar to pay for itself?

Payback periods vary based on system size, utility rates, and the specific incentive combination captured. When federal tax credits, bonus depreciation, and ongoing utility bill savings are factored in, most commercial installations achieve payback in 5–8 years, with systems generating savings for 25 years or more after that.

What happens if construction doesn't begin by July 4, 2026?

For applicable wind and solar facilities under Section 48E, missing the July 4, 2026 construction start deadline means the project must be placed in service by December 31, 2027 to qualify—and projects that miss both deadlines may receive no federal ITC at all. Starting the permitting and contractor engagement process now is the safest way to protect eligibility.