This guide covers everything you need to claim it: what the credit is, who qualifies, what expenses count, how to file, and how California homeowners can layer additional state incentives on top.

TL;DR: Key Takeaways

- The Residential Clean Energy Credit equals 30% of qualifying solar installation costs for systems placed in service by December 31, 2025

- Non-refundable, but any unused credit carries forward to future tax years — so you won't lose it if your tax liability is low

- No income limits — any homeowner who pays federal taxes and owns their system qualifies

- Qualifying costs cover panels, installation labor, battery storage (3+ kWh capacity), and connecting wiring

- To claim it, file IRS Form 5695 with your federal return for the tax year your system was installed

What Is the Residential Clean Energy Credit and How Much Can You Save?

The Residential Clean Energy Credit (IRS Section 25D) is a tax credit, not a deduction. That distinction matters. A deduction reduces your taxable income; a credit reduces your actual tax bill dollar-for-dollar.

Quick example: a $6,000 credit applied to a $10,000 tax bill leaves you owing $4,000.

The 30% Rate — And Why 2025 Is the Deadline

According to the IRS, the credit equals 30% of the cost of new, qualified clean energy property installed from 2022 through December 31, 2025. The One Big Beautiful Bill (P.L. 119-21, passed July 2025) terminated the credit for expenditures made after that date. There's no reduced phase-down rate — post-2025 installations receive no credit at all.

What That Looks Like in Real Dollars

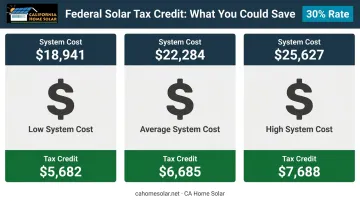

EnergySage data from May 2026 puts the average California residential solar system at 8.81 kW, costing $22,284 before incentives (range: $18,941–$25,627).

Run the math:

| System Cost | Credit Rate | Federal Tax Credit |

|---|---|---|

| $18,941 | 30% | $5,682 |

| $22,284 | 30% | $6,685 |

| $25,627 | 30% | $7,688 |

For most Southern California homeowners, a $6,000–$7,000 credit covers a substantial share of their annual federal tax bill — which is exactly why the December 2025 cutoff makes timing critical.

Non-Refundable but Carries Forward

The credit is non-refundable, meaning it can't push your tax liability below zero or generate a cash refund. Unused amounts carry forward to future tax years, though.

Here's how that works in practice:

- You owe $4,000 in federal taxes this year

- Your credit is $6,685 — you apply the full $4,000 now

- $2,685 carries forward to next year's return

One important note on caps: there's no annual or lifetime dollar limit for solar PV systems. Fuel cell property is capped separately at $500 per 0.5 kW of capacity.

Who Qualifies for the Residential Clean Energy Credit?

Residence and Ownership Requirements

The solar system must be installed at a U.S. home you use as a residence. Eligible property types include houses, condos, mobile homes, manufactured homes, houseboats, and cooperative apartments. A second home or vacation property qualifies if you live there part of the year and don't rent it to others.

You must own the system outright, whether purchased with cash or financed through a loan. If a third-party company owns the panels under a lease or power purchase agreement (PPA), you cannot claim the credit.

Rental and Partial-Use Rules

Ownership alone isn't enough — how you use the property also affects eligibility:

- Landlords who don't personally live in the rental property cannot claim the credit

- Mixed-use homes (part personal, part rental): you can claim a prorated share based on the percentage of the year you personally occupy the home

- Partial business use: if business use is 20% or less, you claim the full credit; above 20%, the credit is limited to the non-business share of costs

Equipment and Timing

The system must be:

- New — used or previously owned equipment doesn't qualify

- Installed and operational by December 31, 2025 — purchased but not yet installed doesn't count

- Claimed for the tax year installation is completed, not when you signed the contract

What Solar Expenses Are Covered Under This Credit?

Eligible Equipment Categories

The IRS recognizes six categories of qualifying property under Section 25D:

- Solar electric panels (photovoltaic systems that generate electricity for your home)

- Solar water heaters (must derive at least 50% of energy from the sun; must be SRCC-certified or equivalent)

- Small wind turbines (generating electricity for residential use)

- Geothermal heat pumps (must meet current Energy Star requirements)

- Fuel cell systems (minimum 0.5 kW capacity, minimum 30% efficiency; capped at $500 per 0.5 kW)

- Battery storage technology (minimum 3 kWh capacity; eligible from 2023 onward)

What Labor and Installation Costs Count

The credit covers more than just equipment. Eligible costs include:

- Onsite preparation and assembly

- Original installation labor

- Piping or wiring to connect the system to your home

Solar roofing tiles and solar shingles that actively generate electricity also qualify — they serve dual roles as both roofing material and solar collector.

What Doesn't Qualify

- Used or previously owned equipment

- Systems that heat swimming pools or hot tubs

- Standard roofing materials or structural components that only support panels (trusses, standard shingles)

- Any costs covered by a public utility subsidy — subtract those from your qualified cost before calculating the credit

Two points are easy to confuse here. Net metering credits — payments from your utility for excess electricity you export to the grid — do not reduce your qualified cost basis. State incentives labeled as "rebates" are a different matter: whether they must be subtracted depends on how they're structured, so confirm the treatment with a tax professional before you file.

How to Claim the Residential Clean Energy Credit: Step-by-Step

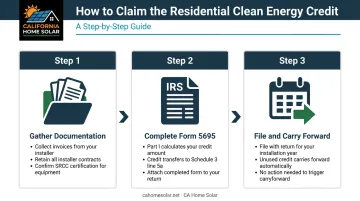

Step 1: Gather Your Documentation

Save every receipt, invoice, and installer contract showing the total cost of equipment and labor. If your system includes solar water heating, you'll need the SRCC certification document. The tax year that matters is the year installation was completed and the system became operational.

Step 2: Complete IRS Form 5695

Form 5695 (Residential Energy Credits) is the required form. Part I calculates your Residential Clean Energy Credit. The final credit amount from line 15 transfers to Schedule 3 (Form 1040), line 5a.

You do not need to itemize deductions to claim this credit — it's available whether you take the standard deduction or itemize.

Step 3: File and Carry Forward if Needed

File Form 5695 with your return for the year the system was placed in service. If your credit exceeds your tax liability, the unused portion carries forward automatically. Recent federal legislation didn't change this — a 2025 Congressional Research Service analysis confirmed the carryforward provision remained intact.

Missed the credit in a prior year? You can file an amended return using Form 1040-X — generally within 3 years of filing the original return or 2 years after paying the tax, whichever is later.

Residential Clean Energy Credit vs. Energy Efficient Home Improvement Credit

These are two separate credits, both calculated on Form 5695, and you can claim both in the same tax year.

| Feature | Residential Clean Energy (25D) | Energy Efficient Home Improvement (25C) |

|---|---|---|

| What it covers | Solar panels, wind, geothermal, battery storage | Windows, doors, insulation, HVAC, water heaters, audits |

| Credit rate | 30% | 30% |

| Dollar cap | None (except fuel cells) | $1,200/year (most items); $2,000 for heat pumps |

| Eligible homes | New and existing | Existing homes only |

| Expires | December 31, 2032 | December 31, 2032 (per the Inflation Reduction Act) |

California Home Solar installs solar systems alongside qualifying HVAC upgrades and energy-efficient windows. Homeowners who bundle these improvements in the same tax year can claim credits under both sections — and neither credit affects the other's calculation or dollar limit.

How Southern California Homeowners Can Maximize Their Solar Tax Benefits

California's Property Tax Exclusion

California offers an active solar energy system new construction exclusion — meaning adding solar to your home won't trigger a property tax reassessment. The exclusion applies to systems installed before January 1, 2027, and in most cases is granted automatically without the homeowner filing a separate application.

Battery Storage: SGIP

California's Self-Generation Incentive Program (SGIP) offers incentives for battery storage systems. SGIP is administered through CPUC and participating utilities. Current status varies by utility:

- SCE: Ratepayer-funded SGIP budgets are currently closed; state-funded Residential Solar and Storage Equity budget is in waitlist status

- LADWP: SGIP funding is available for income-qualified households at or below 80% of Area Median Income

If you do receive a SGIP rebate or any public utility subsidy, the IRS requires you to subtract that amount from your qualified costs before calculating the 30% federal credit.

Net Billing Tariff (NEM 3.0) Context

California replaced NEM 2.0 with the Net Billing Tariff on December 15, 2022, applicable to customers who submitted interconnection applications on or after April 15, 2023 in PG&E, SCE, and SDG&E territories. Under this tariff, export credits are based on the avoided cost to the grid rather than retail rates — generally lower than under NEM 2.0, though higher during peak grid demand hours.

SCE refers to this as the Solar Billing Plan, with Energy Export Credits applied to exported electricity. Key tax credit point: these net billing credits do not reduce your qualified costs for the federal tax credit calculation — your full system cost remains eligible.

Working With the Right Installer

Getting the credit right starts before you even file. Equipment must meet IRS eligibility requirements, costs must be properly documented, and installation must be completed in the qualifying tax year. That means your installer's recordkeeping matters as much as the hardware they put on your roof.

Look for a contractor with demonstrated experience handling the documentation Form 5695 requires. California Home Solar has completed solar installations across Southern California for 36 years and holds Top 500 Solar Contractor recognition from Solar Power World — the kind of track record that translates to installations done correctly the first time, with paperwork to match.

Frequently Asked Questions

Are there tax credits for residential solar panels?

Yes. The federal Residential Clean Energy Credit provides a 30% tax credit on qualifying solar panel installation costs for systems placed in service by December 31, 2025. There's no dollar cap and no income limit.

Is the Residential Clean Energy Credit refundable?

No, the credit is non-refundable. It can reduce your federal tax bill to zero but won't generate a cash refund for any remaining balance. Unused credit carries forward to future tax years.

Can I claim the solar tax credit if I financed my solar panels with a loan?

Yes. Homeowners who purchase solar systems through a traditional loan or solar-specific financing own the system and qualify for the credit. Leased systems and PPAs do not qualify because the third-party company retains ownership.

What form do I file to claim the Residential Clean Energy Credit?

File IRS Form 5695 (Residential Energy Credits) with your annual federal tax return for the year the system was installed. You don't need to itemize deductions to claim it.

Can I carry forward unused solar tax credits to future tax years?

Yes. Any portion of the credit exceeding your tax liability in the installation year carries forward and can be applied to future years. The One Big Beautiful Bill did not change this carryforward provision.

Does California offer additional solar incentives beyond the federal tax credit?

California offers a property tax new construction exclusion for solar systems (through January 1, 2027) and battery storage rebates through SGIP, though availability varies by utility and income eligibility. Net billing credits from your utility don't reduce your federal credit calculation.