The short answer is no, but the full picture is more nuanced. Misunderstanding these rules can lead to overclaimed credits, IRS scrutiny, and unexpected tax bills. Getting it right upfront protects both your finances and your tax return.

This guide covers what the solar tax credit actually covers, which roofing costs may (and may not) qualify, the BIPV exception, and how to document your project properly.

Disclaimer: This article is for informational purposes only. Consult a qualified tax professional for guidance specific to your situation.

Key Takeaways

- The federal Residential Clean Energy Credit offers 30% back on qualifying solar installation costs — but standard roof replacement generally doesn't qualify

- Only solar panels, inverters, wiring, mounting hardware, labor, permits, and qualifying battery storage are eligible

- Structural work specifically required to support solar panels may qualify, but requires careful documentation and professional guidance

- Building-integrated photovoltaics (solar shingles/tiles) can qualify because they function as both roof and solar system

- The 30% credit applies to systems installed through December 31, 2025, after which it phases down

What Is the Federal Solar Tax Credit?

The Residential Clean Energy Credit — the formal name for what most people call the solar ITC — lets homeowners claim 30% of qualifying solar installation costs as a direct credit against federal taxes owed.

Here's how the credit actually works:

- Tax credit vs. deduction: A credit reduces your tax bill dollar-for-dollar. A $10,000 credit means $10,000 less owed — not just a reduction in taxable income

- Nonrefundable: The credit can't reduce your tax liability below zero. If you owe $5,000 but your credit is $8,000, you get the $5,000 — but not a $3,000 refund

- Carryforward: The unused $3,000 carries forward to the following tax year, so you won't lose it

- No dollar cap: There's no annual or lifetime limit on the solar credit (except for fuel cell property)

The 2025 Deadline Matters

The 30% rate applies to systems placed in service through December 31, 2025. Per the Inflation Reduction Act schedule, the rate steps down to 26% in 2033 and 22% in 2034 before expiring in 2035 unless Congress acts. For Los Angeles area homeowners planning a combined roof-and-solar project, that makes 2025 the optimal window. A system must be fully installed and operational — not just contracted or purchased — before December 31 to qualify at the current rate.

Does Roof Replacement Qualify for the Solar Tax Credit?

No. The IRS is explicit: traditional roofing materials and structural components do not qualify for the Residential Clean Energy Credit.

The IRS Energy Incentives FAQ states directly that components such as roof decking or rafters serving only a roofing or structural function are excluded — even when installed in preparation for solar panels.

Where the Confusion Comes From

The Form 5695 instructions include this language: "No costs relating to a solar panel or other property installed as a roof (or portion thereof) will fail to qualify solely because the property constitutes a structural component."

This sentence is frequently misread. It wasn't written to make traditional roofing eligible — it was written to protect building-integrated photovoltaics (solar tiles and shingles that are both roof and solar collector).

That misreading has led some solar contractors to tell homeowners they can claim the full roof replacement under the ITC. That claim is wrong — and the homeowner, not the contractor, bears IRS responsibility if the credit is overclaimed.

Ownership Requirement

To qualify for the ITC at all, you must own both the home and the solar system. Arrangements that disqualify you include:

- Solar leases — the leasing company owns the equipment and claims the credit

- Power purchase agreements (PPAs) — same ownership issue applies

- Rental properties where you don't own the home — ownership of the structure is required

Roof-Related Costs That May Partially Count

While a standard roof replacement doesn't qualify, there are narrow situations where some roof-related work might be includable.

Structural Reinforcements Required for Solar

If an existing roof can't support the weight of solar panels — and new joists, rafters, or decking are required specifically because of the solar installation — the IRS allows you to treat those costs as integral to the solar system rather than general roofing work. Tax publications like The Tax Adviser have referenced an "incremental cost" analysis for such situations.

This is a genuine gray area. If you're pursuing this:

- Get a structural engineer's written assessment documenting why reinforcement is required for solar loading

- Ensure your contractor's invoice separates these costs from general roofing work

- Discuss with a CPA before claiming anything roofing-adjacent on Form 5695

Specialized Components Integral to the Solar System

Mounting substrates or underlayments required by the solar system manufacturer — not standard weatherproofing materials — may be treated separately from general roofing costs if they're functionally part of the installation. Detailed contractor invoices and manufacturer specifications are your best protection if the IRS questions the claim.

The Section 25C Alternative

If you're replacing your roof with energy-efficient materials, a separate credit may apply. The Energy Efficient Home Improvement Credit (Section 25C) offers up to $1,200 annually for qualifying improvements. Under the Inflation Reduction Act, this credit is currently available through December 31, 2032 — giving homeowners a longer runway to plan qualifying upgrades.

Practical recommendation for Southern California homeowners: Get a professional roof inspection before committing to solar installation. CA Home Solar offers both roofing and solar services throughout the Los Angeles area, and getting clearly itemized quotes — with roofing costs and solar costs on separate line items — makes it far easier to substantiate your credit claim if the IRS asks questions.

What IS Fully Covered Under the Solar Tax Credit

The DOE Homeowner's Guide to the Federal Tax Credit and IRS Form 5695 instructions are clear about what qualifies:

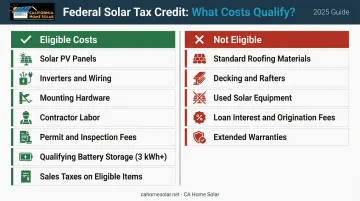

Eligible costs:

- Solar PV panels or cells

- Inverters, wiring, and mounting hardware

- Contractor labor for onsite preparation, assembly, and original installation

- Permitting fees, inspection costs, and developer fees

- Battery storage systems (must have at least 3 kWh capacity and be charged exclusively by solar)

- Sales taxes on all eligible expenses

Not eligible:

- Standard roofing materials, decking, rafters, or structural components serving only a roofing function

- Used or previously owned solar equipment

- Loan interest, origination fees, and extended warranty costs

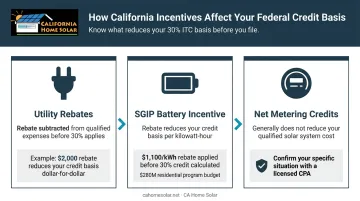

How California Incentives Affect Your Credit

California homeowners need to account for three types of incentives when calculating their Form 5695 basis:

- Utility rebates: Public utility subsidies are subtracted from qualified expenses before you apply the 30% rate. If your utility pays $2,000 directly to your contractor, your eligible cost drops by $2,000 first.

- SGIP battery storage incentives: California's SGIP program falls under similar treatment. The CPUC has authorized $280 million for the Residential Solar and Storage Equity budget, with rates of $1,100/kWh for storage — so an SGIP rebate can meaningfully reduce your credit basis.

- Net metering credits: State-level net metering credits generally don't reduce your qualified cost, though this is worth confirming with your CPA.

If you receive an SGIP rebate, discuss with your tax professional how it affects your Form 5695 basis before filing.

The BIPV Exception: When Your Roof IS the Solar System

Building-integrated photovoltaics (BIPV) are products like solar roof tiles and solar shingles that simultaneously generate electricity and function as roofing material. The IRS has ruled these can qualify for the solar tax credit precisely because they aren't traditional roofing components — they're classified as solar energy generation equipment, not structural roofing.

Two well-known examples are the Tesla Solar Roof and GAF Energy's Timberline Solar ES 2, a nailable solar shingle that delivers 57 watts per unit.

The Allocation Catch

Only the portion of BIPV costs attributable to electricity generation qualifies — not the portion that simply replaces what a traditional roof would provide. The IRS hasn't published a specific formula for this split. In practice, your BIPV manufacturer can provide documentation on the generation-only cost share, and a tax professional can confirm how to apply it on your return.

NREL data puts average installed residential BIPV at roughly $5.02/W, compared to $3.92/W for conventional racked systems. That cost premium is worth weighing against the tax benefit before choosing the BIPV route purely for credit purposes.

How to Claim the Credit and Document Your Project

Filing Basics

- Claim the credit on IRS Form 5695 filed with your federal return

- Claim it for the tax year in which the system is placed in service (fully installed and operational) — not when you signed the contract or made a deposit

- If your credit exceeds your tax liability, the unused portion carries forward to the next year

Documentation That Protects You

The most common audit risk isn't claiming the solar credit itself — it's including ineligible costs. Protect yourself with:

- Itemized invoices that clearly separate solar installation costs from any roofing work

- Permits and inspection records from the installation

- Structural documentation if any roof work is being included as solar-required (engineering assessment confirming the reinforcement was necessary for panel installation)

- Manufacturer specifications if any specialized mounting components are being treated as solar system components

CA Home Solar handles both solar and roofing projects, which matters at tax time. When one contractor manages both scopes, invoices are structured from day one to clearly separate solar costs from roofing costs — exactly what the IRS expects to see.

Before filing, consult a CPA. Carryforward rules, AMT exposure, and your specific tax liability can all shift the math in ways a qualified preparer will catch that standard tax software won't.

Frequently Asked Questions

Can I claim a roof replacement as part of the solar tax credit?

Generally no. Traditional roof replacement costs — shingles, decking, rafters — don't qualify for the federal solar tax credit. Only costs directly tied to the solar system, and in limited cases structural work required to support panel weight, may qualify. Consult a tax professional for your specific situation.

Is $30,000 too much for a roof in Southern California?

Not necessarily. Angi reports the average LA roof replacement costs around $17,271, with larger homes or premium materials easily reaching $25,000–$30,000+. That cost generally won't qualify for the solar ITC, but a separate energy efficiency credit or PACE financing through programs like HERO may help offset it.

What expenses are covered under the federal solar tax credit?

Solar panels, inverters, wiring, mounting hardware, labor for installation, permitting fees, sales taxes on eligible items, and qualifying battery storage (3 kWh minimum capacity). Standard roofing materials and loan interest are excluded.

Do I need to own my solar panels to qualify for the ITC?

Yes. You must purchase the system outright — with cash or a loan. Leased panels or those under a power purchase agreement (PPA) don't qualify because the leasing company retains ownership and claims the credit instead.

What are building-integrated photovoltaics, and do they qualify?

BIPVs are products like solar shingles and solar roof tiles that do double duty — generating electricity while acting as roofing material. Because they function as solar generation equipment rather than standard roofing, they can qualify for the solar tax credit.

Can I carry forward the solar tax credit if I don't owe enough taxes?

Yes. The Residential Clean Energy Credit is nonrefundable, meaning it can't reduce your tax bill below zero. Any unused portion carries forward to future tax years until the full credit is applied.