The short answer: solar panels don't automatically spike your premiums, but they can under certain conditions. The longer answer depends on your coverage limits, how your panels are mounted, whether you own or lease them, and the increasingly complex insurance landscape specific to California.

This guide breaks down exactly when and why costs change, what your existing policy likely covers, and what steps to take before and after installation to protect your investment.

Key Takeaways

- Solar panels don't automatically raise premiums—but may if they push replacement cost above your coverage limit

- Rooftop panels fall under dwelling coverage; ground-mounted panels fall under "other structures," capped at 10% of dwelling coverage

- California's insurance crisis means some homeowners—especially in wildfire zones—need to verify solar coverage explicitly

- Leased panels are generally insured by the solar company, not you—but check your lease

- Notify your insurer before installation and update your coverage limit to avoid gaps

Do Solar Panels Increase Home Insurance Premiums?

The direct answer: not always, but often somewhat.

The driving factor is whether your solar system pushes your home's total replacement cost above your current coverage limit. If your dwelling coverage already falls short of your home's true rebuild cost, adding solar means you'll likely need to raise that limit—and that's what raises your premium.

When Premiums Change—and When They Don't

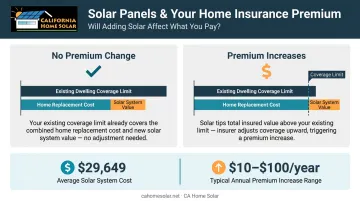

- Premiums stay the same if your current dwelling limit already exceeds your home's replacement value plus the solar system cost. No limit adjustment needed, no premium change.

- Premiums increase if the solar system tips your total replacement cost above your existing limit—you'll need to raise coverage, which costs more.

According to EnergySage, the average residential solar system costs $29,649 in 2025. That's a meaningful addition to your home's replacement value, and it's worth recalculating your dwelling limit when you install.

One insurer source (NJM) cites premium increases of roughly $10 to $100 per year when coverage adjustments are needed. The actual figure depends on your system size, your current insurer, and how much your limit needs to rise.

The Home Value Connection

Zillow Research found in 2019 that homes with solar sold for 4.1% more than comparable homes without—roughly $9,274 on a median-valued home. Higher home value translates to higher replacement cost, which can ripple into insurance costs over time as your policy is reviewed or renewed.

Any premium increase is typically modest compared to the long-term energy savings solar delivers. Still, recalculate your dwelling coverage before installation so the adjustment doesn't catch you off guard at renewal.

What Homeowners Insurance Typically Covers (and Doesn't)

Rooftop vs. Ground-Mounted Systems

How your panels are mounted determines which part of your policy applies:

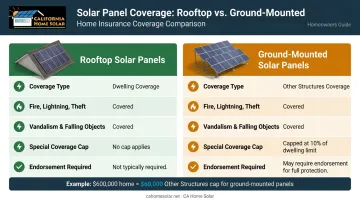

- Rooftop panels are generally treated as a permanent part of your home's structure, covered under dwelling coverage for standard perils—fire, lightning, theft, vandalism, and falling objects

- Ground-mounted panels (and solar carports) aren't attached to the main structure, so they typically fall under "other structures" coverage, which is commonly capped at 10% of your dwelling coverage limit

That 10% cap matters. If your home is insured for $600,000, your other structures coverage may only be $60,000, which may not be enough to replace a large ground-mounted system.

CA Home Solar installs ground-mount systems throughout Southern California. Homeowners choosing that option should verify their other structures limit before installation and consider requesting an endorsement if the standard limit falls short.

Common Exclusions to Watch For

Standard homeowners policies don't cover everything. Watch for these gaps:

- Wear and tear or maintenance issues — not a covered peril; that's on you

- Manufacturer defects — covered by equipment warranties, not home insurance

- Wind and hail damage — some policies specifically exclude this for solar panels; check yours

- Improper installation damage — often the most costly gap, covered separately below

The Workmanship Gap

That last exclusion deserves a closer look. Standard homeowners insurance does not cover workmanship damage — meaning roof leaks or structural issues caused by faulty panel installation. If panels are incorrectly mounted and water intrudes through a roof penetration, that's not a covered peril; it's the installer's responsibility.

This is why installer credentials matter as much as your insurance policy. CA Home Solar has 36 years of experience in Southern California and holds Top 500 Solar Contractor recognition—the kind of track record that reduces workmanship risk from the start. Before signing with any installer, confirm they carry general liability insurance and offer a workmanship warranty.

California-Specific Insurance Considerations

Southern California homeowners face insurance challenges that don't exist in most other states. Getting ahead of them before installation can prevent costly coverage gaps.

The California Insurance Crisis

Major insurers have retreated significantly from the California market due to wildfire risk:

- State Farm stopped accepting new California property and casualty applications effective May 27, 2023

- Allstate stopped selling new California home policies, also in 2023

- Fortune reported four more insurers pulled out or cut back by October 2023

Many homeowners in LA County, Malibu, the Antelope Valley, Palmdale, and Lancaster may already be on limited policies or the California FAIR Plan (the state's insurer of last resort).

FAIR Plan policies offer basic named-peril dwelling coverage, but official documents don't explicitly spell out how attached or detached solar equipment is treated. If you're on a FAIR Plan, ask your broker directly how solar panels would be handled before you install.

Earthquake Coverage: A Separate Conversation

Standard homeowners insurance does not cover earthquake damage in California—that's a separate policy, typically through the California Earthquake Authority (CEA). If your solar panels are damaged in a seismic event, your homeowners policy won't respond. CEA policy documents don't explicitly address solar panels in most cases, so confirm solar coverage directly with your earthquake insurer before you install.

Wildfire risk creates a similar gap—insurers in high-hazard zones often treat solar equipment differently than the rest of your dwelling coverage.

Wildfire Zones and Solar Coverage

If your home is in a designated Fire Hazard Severity Zone—common across much of Southern California—some insurers may:

- Charge higher premiums or require endorsements to cover solar panels against fire damage

- Restrict coverage in ways that affect how solar equipment is treated

NEM 3.0 Registration

California's Net Billing Tariff (NEM 3.0) applies to interconnection applications submitted after April 14, 2023. At installation, two parallel steps are required:

- Register your system with your utility as part of the interconnection process

- Notify your insurer so your policy reflects the added value

Owned vs. Leased Solar Panels: How It Affects Coverage

Ownership structure changes who insures your system.

| Scenario | Who Insures the Panels |

|---|---|

| Purchased outright or via solar loan | You—panels are part of your home; add to dwelling coverage |

| Leased / Power Purchase Agreement (PPA) | Solar company typically insures their own equipment |

| HERO/PACE financing | You own the panels; confirm coverage with your insurer |

Here's how each scenario plays out in practice.

Owned systems (purchased or financed via a solar loan) become part of your home. Notify your insurer, confirm dwelling coverage limits, and make sure the system value is reflected in your policy.

Leased systems are technically owned by the solar company. Their insurance typically covers the equipment. That said, some leasing contracts require the homeowner to maintain coverage. Read the insurance clause in your lease agreement carefully before assuming coverage is handled.

HERO/PACE financing works differently: PACE creates a property tax assessment and a lien on your property, but you own the panels. California Home Solar is a HERO Registered Contractor, so some customers finance their systems this way.

Because the panels remain tied to the property title, homeowners using PACE should confirm with their insurer that coverage is properly set up. The financing structure itself doesn't change what perils are covered, but the lien does affect title and resale considerations.

Steps to Protect Your Coverage Before and After Installation

Getting your insurance right means acting before the installation crew shows up, not scrambling afterward.

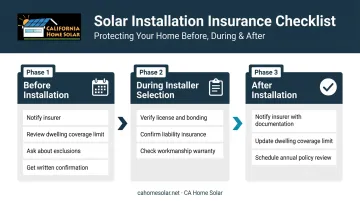

Before installation:

- Contact your insurer to notify them of your plans

- Review your current dwelling coverage limit against your home's actual replacement cost

- Ask specifically about exclusions—wind, hail, ground-mount systems

- Get written confirmation of how the new system will be covered

Your contractor choice directly affects both the quality of installation and your coverage eligibility.

During installer selection:

- Choose a licensed, bonded contractor that carries its own liability insurance

- Confirm the installer offers a workmanship warranty

- Verify the contractor has local experience with Southern California permitting and utility interconnection requirements

After installation:

- Notify your insurer with documentation: system cost, equipment specs, installation records

- Update your dwelling coverage limit if the system's replacement value requires it

- Review your policy annually—home values and panel replacement costs change over time

Do You Need a Separate Solar Panel Insurance Policy?

For most homeowners with a rooftop system, no—adjusting your existing homeowners policy is sufficient. A standalone solar insurance policy is worth considering in specific situations:

- Your system is very large or has high replacement value

- You have a ground-mounted system that exceeds the 10% other structures limit

- Your existing insurer offers limited or uncertain coverage in a high-risk California zone

How Warranties Complement Insurance

Your installer and manufacturer warranties handle the things home insurance won't touch:

- Equipment/product warranties cover manufacturer defects for 10–12 years

- Performance warranties guarantee energy output levels for 20–25 years

- Workmanship warranties cover installation errors for 1–10 years, depending on the installer

Warranties aren't a substitute for insurance—they address defects and installation quality, while insurance addresses perils like fire or theft. Before your system goes live, confirm both are in place so there's no gap if something goes wrong.

Frequently Asked Questions

Should I add my solar panels to my home insurance?

Yes—notify your insurer when you install and confirm coverage is in place. If the panels' replacement cost pushes your home's total value above your existing policy limit, you could be underinsured without realizing it. Get written confirmation from your insurer.

How much will my home insurance premium increase after installing solar panels?

It varies. One insurer source cites roughly $10 to $100 per year when coverage adjustments are needed. The amount depends on your system size, your insurer, and whether your dwelling limit needs to increase. Request a specific quote from your insurer before installation.

Does homeowners insurance cover solar panel damage from wildfires?

Fire is typically a covered homeowners peril, and rooftop panels treated as dwelling property would generally be subject to that coverage. California homeowners—especially those on a FAIR Plan or in high-risk wildfire zones—should verify this directly with their insurer before installation.

What happens to my insurance if I lease solar panels instead of buying them?

Leased panels are typically covered by the solar company's insurance since they own the equipment. However, some lease agreements require the homeowner to carry coverage—review your lease contract's insurance clause carefully before assuming full coverage.

Does homeowners insurance cover roof damage caused during solar panel installation?

No—standard homeowners insurance does not cover installation-related roof damage. This is a workmanship issue, not a covered peril. Choose an installer that carries general liability insurance and offers a workmanship warranty to protect yourself if damage occurs.

Are ground-mounted solar panels covered by homeowners insurance?

Ground-mounted panels typically fall under "other structures" coverage, which is commonly capped at 10% of your dwelling coverage limit. If your system's replacement value exceeds that cap, you may need to add an endorsement or separate policy for full protection.