The federal tax code offers two powerful tools: the Section 179D energy efficiency deduction and the Section 48 Investment Tax Credit. Layer those on top of California utility rebates from SCE and SoCalGas, and the effective net cost of a qualifying HVAC upgrade drops considerably. The catch? Each incentive has its own eligibility rules, documentation requirements, and deadlines — and most property owners discover them too late.

This guide breaks down each available incentive, explains which HVAC systems qualify, and shows how to stack them on a single project.

Key Takeaways

- Section 179D deducts up to $5.94/sq ft (2026, with prevailing wage compliance) for energy-efficient commercial HVAC upgrades

- Section 48 ITC offers a 30% direct credit for qualifying equipment like geothermal heat pumps; standard RTUs and VRF systems don't qualify

- SCE commercial rebates cover RTUs, VRF systems, and controls, up to $200/ton for top-tier equipment; pre-installation reservation required

- Incentives can be stacked, but each has separate eligibility rules; a tax professional familiar with energy credits is essential

- Systems must be placed in service before December 31 of the tax year you want to claim

Federal Tax Credits and Deductions for Commercial HVAC Upgrades

Section 179D: The Most Valuable Federal Incentive

Section 179D (significantly expanded by the Inflation Reduction Act) provides a direct tax deduction — not a credit — for energy-efficient upgrades to commercial buildings, including HVAC systems.

According to IRS Form 7205 instructions, the 2026 deduction rates are:

| Compliance Level | Deduction Range (per sq ft) |

|---|---|

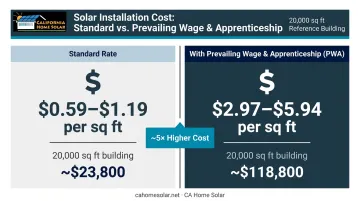

| Standard rate | $0.59 – $1.19 |

| With Prevailing Wage & Apprenticeship (PWA) | $2.97 – $5.94 |

The difference between standard and PWA rates is substantial. On a 20,000 sq ft building, the gap between a $1.19 deduction and a $5.94 deduction is the difference between roughly $23,800 and $118,800. Choosing the right compliance path before construction begins is worth the extra planning effort.

Who qualifies:

- Commercial building owners

- Certain tenants who pay for the improvements

- Tax-exempt building owners can allocate the deduction to the qualifying designer or contractor

Critical eligibility requirement: The upgrade must reduce the building's total annual energy costs by at least 25% compared to the applicable ASHRAE 90.1 baseline standard. Simply buying a high-efficiency unit isn't enough — you need a certified energy model to prove the threshold is met.

The deduction is taken in the year the system is placed in service, which means faster tax relief than standard depreciation schedules. One important note: IRS Form 7205 instructions state that Section 179D is terminated for property where construction begins after June 30, 2026 — so timing matters.

Section 48 Investment Tax Credit

Section 48 ITC provides a direct credit against your tax liability — dollar-for-dollar reduction in taxes owed, not just taxable income. That distinction makes it more immediately valuable for property owners with significant tax exposure.

The base credit rate is 6%, rising to 30% when prevailing wage and apprenticeship requirements are met.

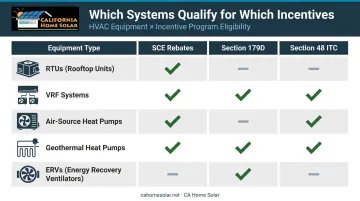

Standard commercial HVAC equipment — rooftop units, air-source heat pumps, VRF systems — generally does not qualify as standalone Section 48 energy property under December 2024 final regulations.

Equipment that does qualify includes:

- Geothermal heat pump systems

- Thermal energy storage directly connected to HVAC

- Combined heat and power (CHP) systems

- Waste energy recovery property

If your project involves geothermal or thermal storage, Section 48 can stack with 179D. If you're installing a standard RTU or VRF, your federal incentive path runs primarily through 179D and depreciation.

Bonus Depreciation Under Section 168

Beyond credits and deductions, HVAC equipment can deliver a third layer of tax savings through accelerated first-year depreciation. Under IRS Notice 2026-11, 100% bonus depreciation is now permanent for qualified property acquired and placed in service after January 19, 2025 — reversing the prior phase-down schedule that had dropped to 40% in 2025.

Section 179 expensing is another option for smaller commercial properties, with a 2026 deduction cap of $2,560,000 (phased out above $4,090,000 of qualifying property placed in service).

The IRS requires basis reduction by the 179D deduction amount, which affects your depreciation calculation. These incentives aren't entirely additive — work through the math with a tax advisor before assuming you can take all of them at full value simultaneously.

California-Specific Incentives and Utility Rebates

SCE Commercial Rebate Programs

Southern California Edison, through its Commercial Energy Efficiency Program administered by Willdan, offers rebates for qualifying HVAC upgrades. Funds are limited and first-come, first-served — which means pre-installation reservation is required, not optional.

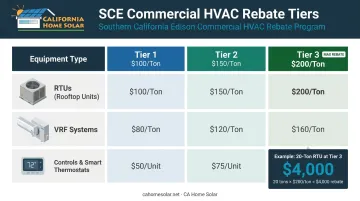

2025 SCE/Willdan commercial HVAC rebates:

| Equipment | Tier 1 | Tier 2 | Tier 3 |

|---|---|---|---|

| Packaged RTU or heat pump (65,000–249,999 Btu/h) | $100/ton | $150/ton | $200/ton |

| Packaged RTU or heat pump (250,000–759,999 Btu/h) | $75/ton | $125/ton | $175/ton |

| Air-cooled VRF | $100/ton | $150/ton | $200/ton |

| Smart thermostats | $50/unit | — | — |

| Advanced RTU controllers | $200/unit | — | — |

For a 20-ton commercial rooftop replacement qualifying at Tier 3, that's $4,000 back before any federal benefit is applied.

SoCalGas and Broader California Programs

If your building relies on gas heating, SoCalGas runs a separate commercial rebate program covering boilers, steam systems, and related thermal measures. Electric heat pumps, RTUs, and VRF systems fall outside the 2026 SoCalGas Business Rebate Guide. For gas heating systems, the program caps at $500,000 per site and $1,000,000 per customer annually.

Beyond utility programs, California offers additional financing channels:

- GoGreen Business Financing (CHEEF): State-backed financing for commercial energy efficiency projects, administered through the California Hub for Energy Efficiency Financing

- CPUC On-Bill Financing: Covers non-residential customers; expanded in 2023 to include additional utility programs

- PACE Financing: Property-Assessed Clean Energy financing is available in California for commercial HVAC improvements through programs like Ygrene, with repayment through property taxes rather than upfront capital

California Home Solar is a HERO Registered Contractor, which means clients exploring PACE-style financing can move forward without tying up capital while waiting for tax benefits at year-end. For smaller commercial portfolios where cash flow timing matters, that separation between project cost and tax benefit timing is often what makes an upgrade feasible.

Which Commercial HVAC Systems Qualify for Tax Credits

Not all equipment qualifies equally, and the distinction between "energy-efficient" and "incentive-eligible" matters more than most property owners realize.

Systems most likely to qualify across multiple programs:

- High-efficiency packaged rooftop units (RTUs) meeting ENERGY STAR or SEER2/EER thresholds

- Variable refrigerant flow (VRF) systems

- Air-source heat pumps (for SCE rebates and potentially 179D)

- Geothermal heat pumps (Section 48 ITC eligible)

- Energy recovery ventilators (ERVs) contributing to building-wide efficiency

For SCE rebates, equipment must meet tiered efficiency thresholds — Tier 3 requires the highest ratings and returns the largest rebate per ton.

For Section 179D specifically, equipment qualification is performance-based, not equipment-list based. The building must be certified to reduce total annual energy costs by at least 25% versus the ASHRAE 90.1 reference standard.

The applicable standard depends on when construction began:

- Pre-January 1, 2023: Reference is ASHRAE 90.1-2007

- On or after January 1, 2023 (placed in service before January 1, 2027): Reference is ASHRAE 90.1-2019

You can't simply pull the ENERGY STAR certificate off a new unit and claim 179D. You need a formal energy model, certified by a qualified engineer, showing the required percentage reduction across building systems.

IRA Rule Change (Post-2022): The IRA eliminated the old partial deduction and interim lighting rules for property placed in service after December 31, 2022. If your upgrade straddles that date, confirm which rules apply before filing.

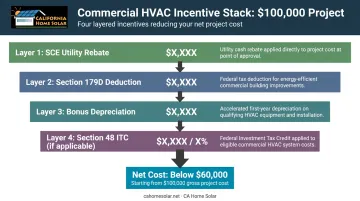

How to Stack and Maximize Multiple Incentives

Commercial HVAC upgrades qualify for multiple incentives simultaneously. Used together, they can dramatically reduce your net project cost.

The Stacking Framework

Consider a hypothetical $100,000 commercial HVAC project (this is illustrative, not a guarantee of any specific outcome):

- SCE utility rebate (applied pre-installation): Reduces upfront cost or is received shortly after installation

- Section 179D deduction: Claimed at year-end filing; reduces taxable income based on building square footage and efficiency certification

- Bonus depreciation: Further deduction in year one on the remaining equipment basis after 179D basis reduction

- Section 48 ITC (if geothermal or thermal storage is included): Direct credit against tax liability

Each layer reduces the effective net cost independently. On a large commercial building, layering all four can bring a $100,000 project's after-tax cost well below $60,000 — even without a geothermal component.

Timing Strategy

Sequencing matters as much as stacking:

- Apply for SCE rebates before installation begins — reservation is required, and funds deplete

- Schedule installation to be placed in service before December 31 of the tax year you want to claim

- Commission the energy model and 179D certification during or immediately after installation, not months later

- File Form 7205 with your tax return for the year the system is placed in service

SoCalGas requires equipment to be installed and in use before submitting the rebate application, with a January 31, 2027 deadline for 2026 business rebates.

Prevailing Wage Requirements

Prevailing wage compliance directly affects how much 179D you can claim — and it must be locked in before work begins, not after.

| Rate Type | Max Deduction |

|---|---|

| Standard 179D | $1.19/sq ft |

| PWA-Compliant 179D | $5.94/sq ft |

To qualify for the enhanced rate, laborers and mechanics must be paid at prevailing wages set by the Secretary of Labor, and apprenticeship labor-hours must equal at least 15% of total hours (for construction starting after December 31, 2023).

For LA-area commercial property owners, this means confirming early that your installing contractor participates in a registered apprenticeship program. It's not something you can add retroactively.

Portfolio Consideration

Section 179D applies per qualifying building. For commercial real estate investors owning multiple properties in the Los Angeles area, each qualifying building is evaluated separately — meaning a portfolio-wide HVAC upgrade program can generate 179D deductions across every compliant property simultaneously.

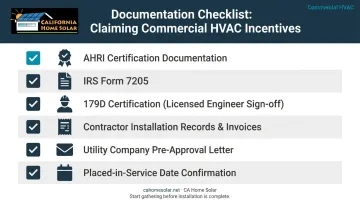

Steps to Document and Claim Your Commercial HVAC Tax Credits

Getting the incentives right starts with documentation, and documentation starts before installation is complete.

Core documentation checklist:

- AHRI certificates confirming equipment efficiency ratings (searchable at the AHRI Directory)

- IRS Form 7205 to calculate and claim Section 179D for property placed in service during the tax year

- A 179D certification from a qualified engineer — a formal energy model confirming the 25% energy cost reduction against ASHRAE 90.1

- Contractor invoices listing equipment model numbers and installation date

- Utility rebate pre-approval letters (SCE) or confirmation of application submission

- Placed-in-service documentation confirming when the system became ready and available for use

The 179D certification is a legal requirement, not optional. A qualified individual must certify the required energy cost reduction — self-certification is not accepted by the IRS. Budget for this cost as part of the project; it typically pays for itself many times over through accurate credit maximization.

Working with a licensed, experienced contractor reduces the documentation burden. CA Home Solar has 36 years of experience serving commercial clients across the Los Angeles area and understands the installation standards that incentive programs require. An experienced contractor ensures the installation meets code, efficiency thresholds, and the documentation standards that rebate programs and the IRS expect.

That contractor knowledge only goes so far, though. Pair it with a CPA or tax advisor who specializes in energy incentives, not a generalist. Claiming Section 179D with incorrect basis calculations or missing certifications results in credit denial, and amended returns create additional complexity and cost.

Frequently Asked Questions

What is the Section 179D deduction and how much can commercial property owners claim?

Section 179D is a federal tax deduction — not a credit — for energy-efficient commercial building upgrades including HVAC, calculated by square footage. For 2026, the standard rate is $0.59–$1.19/sq ft, rising to $2.97–$5.94/sq ft when prevailing wage and apprenticeship requirements are met. The deduction is claimed in the year the system is placed in service.

Can commercial property owners combine federal tax credits with California utility rebates?

Yes — federal incentives (179D, ITC, bonus depreciation) and California utility rebates from SCE or SoCalGas can generally be applied to the same project. Utility rebates may affect your taxable income depending on how they're treated, so confirm the specific tax treatment with a CPA familiar with energy incentives.

What HVAC systems qualify for the federal Investment Tax Credit?

Under Section 48, qualifying commercial HVAC equipment is narrower than most owners expect: geothermal heat pumps, thermal energy storage connected to HVAC, and combined heat and power systems are eligible. Standard air-source RTUs, VRF systems, and conventional heat pumps generally don't qualify as standalone Section 48 property — confirm specifics with a tax professional.

Do I need a third-party energy study to claim Section 179D?

Yes. Section 179D requires certification from a qualified engineer or energy modeler confirming the upgrade meets the 25% energy cost reduction threshold compared to the applicable ASHRAE 90.1 baseline standard. You cannot self-certify, so plan to include this certification cost in your project budget from the start.

When is the best time of year to install commercial HVAC to maximize tax benefits?

Systems must be placed in service before December 31 to claim that year's deduction or credit. For SCE rebates, pre-installation reservation is required and funds are first-come, first-served — so earlier in the year is better. SoCalGas requires equipment to be installed and in use before application submission.

Does using PACE or HERO financing affect eligibility for tax credits or rebates?

No — financing method doesn't affect eligibility for federal tax credits or California utility rebates. What determines eligibility is equipment qualification, installation compliance, and meeting efficiency thresholds.