The good news: you don't need to pay cash to go solar. Five distinct financing structures exist, each with different implications for ownership, tax benefits, and long-term savings. The right choice depends on your financial situation, tax liability, and business goals — not just your budget.

This guide covers all five options, the federal and California-specific incentives that affect your decision, and a practical framework for choosing the right structure.

Key Takeaways

- Cash purchase delivers the highest ROI and full tax benefit eligibility, but requires significant upfront capital

- Solar loans allow ownership with little or no down payment, preserving ITC and depreciation benefits

- PPAs and leases require zero upfront cost — a third party owns the system and handles maintenance

- C-PACE financing uses property value (not credit score) for long-term, 100% financing

- NEM 3.0 and SGIP both affect ROI calculations for California businesses, so understanding each program is essential before selecting a financing structure

Why Commercial Solar Financing Matters for California Businesses

Scale is the first thing to understand. According to LBNL's Tracking the Sun 2024 report, the median installed price for small non-residential systems in California is $3.50/watt, with large non-residential systems averaging $2.50/watt. Average commercial system sizes reach 229 kW — meaning a mid-size commercial installation can easily run $300,000–$600,000 before incentives.

CA Home Solar has completed commercial installations at this scale, including a 240 kW system in Pacoima — a size that illustrates why financing strategy matters as much as system design.

Four Decisions Hidden Inside Your Financing Choice

Four Decisions Hidden Inside Your Financing Choice

Choosing a financing structure determines four outcomes that go well beyond monthly payment size:

- Who controls the system — and who makes future decisions about upgrades, sale, or removal

- Who claims the 30% federal ITC — the tax credit belongs to the system's tax owner, not necessarily the business using it

- How the investment hits your books — as a capital expense, loan obligation, or operating line item

- What you hold at contract end — a paid-off asset or a lease renewal decision on someone else's equipment

Two businesses with identical utility bills and system sizes can end up in very different financial positions. The gap usually comes down to one thing: which structure they chose before signing.

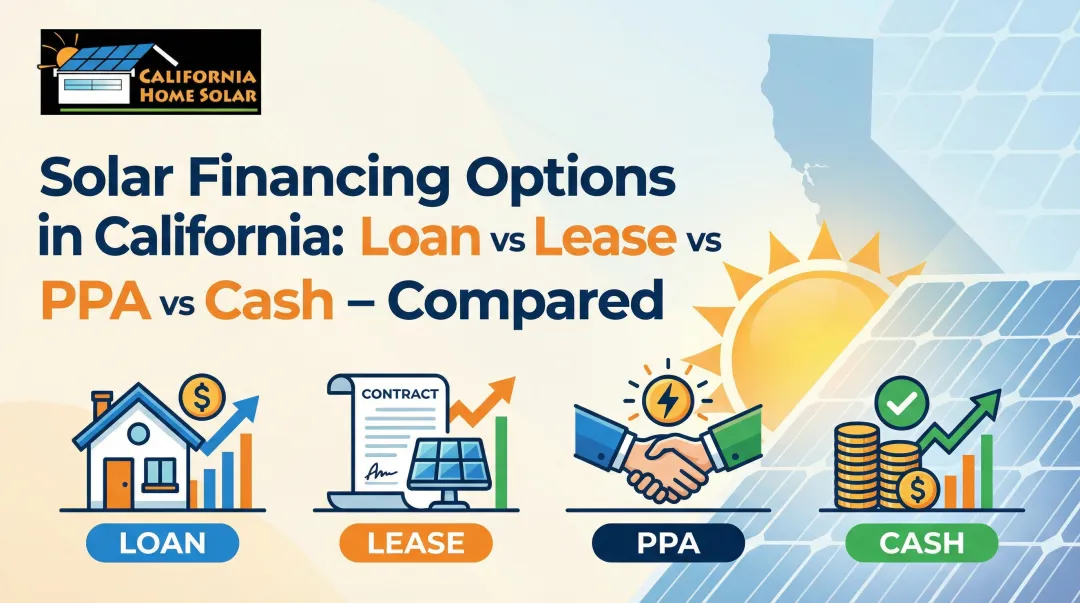

The 5 Commercial Solar Financing Options Explained

Cash Purchase

A direct cash purchase means paying the full system cost upfront, taking immediate ownership, and assuming responsibility for operations and maintenance. In exchange, you get the best possible return on investment.

Why cash wins on ROI:

- No financing costs reduce total savings

- Full eligibility for the 30% federal Investment Tax Credit

- Full access to MACRS 5-year accelerated depreciation

- No long-term contractual obligations to a third party

Payback periods for owned commercial systems typically fall in the 4–7 year range, after which the system generates effectively free electricity for the remainder of its 25+ year lifespan.

One note specific to California: the state no longer has an active SREC market. Post-NEM 3.0, commercial solar owners earn export compensation through the Net Billing Tariff, with credits tied to the CPUC Avoided Cost Calculator rather than retail rates. Factor this into your ROI modeling.

Best for: Businesses with available capital that want maximum long-term savings and full tax benefit eligibility.

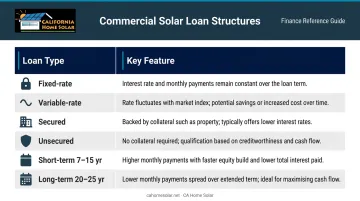

Solar Loans

Solar loans let businesses achieve ownership — and all its tax advantages — with little or no upfront cost. Loan structures vary considerably:

| Structure | Key Feature |

|---|---|

| Fixed-rate | Predictable payments; easier to model ROI |

| Variable-rate | Lower initial rate; payment risk over time |

| Secured | Lower interest rate; tied to property or system |

| Unsecured | No collateral required; higher rate |

| Short-term (7–15 yr) | Higher payments; less total interest |

| Long-term (20–25 yr) | Lower payments; more total interest |

ITC-optimized structures are worth understanding. Because the 30% ITC generates a significant tax credit in year one, some lenders offer re-amortization options (meaning the borrower applies the ITC proceeds as a lump-sum principal reduction, then requests recalculated payments at a lower level). Bridge loans are also used in commercial solar finance, typically advancing around 80% of the expected credit value, with repayment from tax credit proceeds.

Best for: Businesses that want ownership benefits and tax credit eligibility without tying up capital.

Power Purchase Agreements (PPAs)

Under a PPA, a third-party developer installs, owns, and maintains the solar system on your property at no upfront cost. You simply buy the electricity the system generates, typically at a rate below what your utility charges.

Key tradeoffs:

- ✅ Zero upfront investment

- ✅ No maintenance responsibility

- ✅ Predictable electricity cost (often with an annual escalator)

- ❌ The developer — not your business — claims the ITC and depreciation

- ❌ Long contract terms (10–25 years) with limited flexibility

- ❌ Buyout options exist at contract milestones, but at fair market value

PPAs work well for businesses with low or no tax liability (nonprofits, some public institutions) or those prioritizing operating expense predictability over ownership returns. SEIA's commercial PPA framework confirms the developer retains RECs and tax incentives as the system's tax owner.

Best for: Low-tax-liability organizations, businesses wanting zero maintenance responsibility, and those prioritizing budget predictability.

Solar Leases

The key difference between a solar lease and a PPA comes down to billing: instead of paying per kilowatt-hour generated, you pay a fixed monthly amount for the right to use the system. Simpler for budgeting — but with some meaningful tradeoffs.

Operating lease vs. capital lease:

- Operating lease — the lessor retains ownership, claims the ITC and depreciation, and handles maintenance. The business records it as an operating expense.

- Capital lease — the system appears on your balance sheet as an asset; tax treatment varies and requires confirmation from a tax advisor.

Fixed payments are predictable, but under an operating lease the business forfeits the ITC and accelerated depreciation entirely.

CA Home Solar generally steers commercial clients toward purchase options over leases for two reasons: leased systems typically generate lower long-term savings, and they can complicate property sales if the lease term hasn't ended.

Best for: Businesses that cannot access tax credits and prefer simple, fixed monthly costs over ownership complexity.

C-PACE Financing

Commercial Property Assessed Clean Energy (C-PACE) is a government-enabled financing structure that lets businesses fund solar through a voluntary assessment added to their property tax bill.

C-PACE advantages in California:

- 100% upfront financing — no down payment required

- Terms up to 30 years at fixed interest rates

- Qualification based on property value, not credit score (LTV and DSCR metrics apply)

- Assessment transfers with the property on sale — the new owner assumes the obligation

California is an active C-PACE state. Programs operate through administrators including WRCOG for Southern California commercial properties and LA County's PACE program. The California C-PACE program confirms LTV caps of 35% for retrofits and 30% for new construction.

Because the commercial property owner retains system ownership under C-PACE, ITC and MACRS eligibility are preserved. Confirm your tax owner status with a tax advisor before filing to ensure you qualify.

Best for: Commercial property owners with equity in their building who want long-term financing without credit score barriers.

Tax Credits and California Incentives That Affect Your Financing Decision

Federal ITC and MACRS Depreciation

The 30% Investment Tax Credit is the most significant incentive in commercial solar finance. System owners can deduct 30% of total installation cost from federal income taxes in the year the system is placed in service. Under current law, this rate applies to systems placed in service through at least 2032 — see the IRS Clean Electricity Investment Credit for current guidance.

MACRS accelerated depreciation adds substantial value on top. Qualifying commercial solar equipment uses a 5-year cost recovery period. When both incentives are stacked, DOE's worked example shows a $1,000,000 system generating approximately $392,820 in reduced first-year tax liability through the combined effect of ITC and accelerated depreciation assumptions.

One important detail: when claiming the 30% ITC, the depreciable basis is reduced by half the ITC value, leaving 85% of system cost as depreciable basis under MACRS.

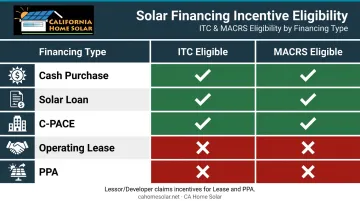

Who can claim these benefits:

| Financing Type | ITC Eligible? | MACRS Eligible? |

|---|---|---|

| Cash purchase | ✅ Yes | ✅ Yes |

| Solar loan | ✅ Yes | ✅ Yes |

| C-PACE | ✅ Yes (confirm with tax advisor) | ✅ Yes |

| Operating lease | ❌ No (lessor claims it) | ❌ No |

| PPA | ❌ No (developer claims it) | ❌ No |

California-Specific Programs

SGIP (Self-Generation Incentive Program): California's incentive for battery storage paired with solar. CPUC administers SGIP through SCE, PG&E, SoCalGas, and LADWP. Current large-scale storage incentives run at $0.25/Wh (or $0.18/Wh for Energy Storage + ITC combinations), though available funding and step status change regularly — verify current availability at the SGIP Program Metrics page before planning.

NEM 3.0 / Net Billing Tariff: Businesses applying for interconnection after April 14, 2023 in SCE territory fall under the Net Billing Tariff. Export compensation now uses CPUC Avoided Cost Calculator values, typically lower than import rates. This shifts solar ROI calculations compared to prior NEM 2.0 treatment, and generally makes battery storage a more attractive pairing. LADWP operates separately under its own commercial solar programs and is not subject to SCE's tariff.

PACE Financing Programs: California remains an active PACE state with commercial programs available through LA County and WRCOG. Note that the HERO program as originally administered by Renovate America is no longer active (the company withdrew from the market in 2020). Current PACE options for Southern California commercial property owners operate through other administrators.

California Home Solar holds HERO Registered Contractor status and works directly with clients to identify which current PACE programs are available for their property and service territory.

Utility rebates: Beyond PACE, direct utility rebates are limited. The California Solar Initiative's general market program closed in 2016, and no current direct SCE commercial PV rebates are confirmed. SGIP for storage and LADWP's commercial programs remain the primary utility-side incentives to verify for your service territory.

How to Choose the Right Commercial Solar Financing Option

Start with four questions:

- Do you want to own the system and claim tax credits? → Cash purchase or solar loan

- Is your tax liability low or zero? → PPA or operating lease

- Do you want to preserve cash and qualify through property equity? → C-PACE or current PACE programs

- Is your priority immediate savings with zero maintenance responsibility? → PPA

Your Real Estate Status Narrows the Field First

Before any financial modeling, your property situation eliminates certain options:

- You lease (don't own) your commercial space — PACE programs are unavailable. PPAs and leases require landlord cooperation and may face approval challenges.

- You own the property with substantial equity — C-PACE becomes highly accessible regardless of your credit profile.

- You own the property outright or with low LTV — the full menu of options is available.

Avoid the "Lowest Upfront Cost" Trap

A PPA may feel free at the start. It isn't. Buying electricity at a contracted rate for 20+ years — in a state where commercial rates are already twice the national average and continuing to rise — often costs more over the system's lifetime than ownership financing would have. The comparison isn't between "free" and "expensive." It's between different total cost profiles over two decades.

Getting that comparison right requires a facility assessment, not a brochure. CA Home Solar — a Top 500 Solar Contractor recognized by Solar Power World with 36 years of commercial solar experience across Southern California — conducts full financial analysis for commercial clients before any contract is signed. That means system design, incentive stacking, and financing fit reviewed together, so the numbers reflect your actual building, usage profile, and ownership structure.

Frequently Asked Questions

How are solar projects financed?

Commercial solar projects are typically financed through one of five structures: cash purchase, solar loan, power purchase agreement, solar lease, or C-PACE/PACE financing. Each affects upfront cost, ownership, tax credit eligibility, and long-term savings differently.

Is commercial solar worth it?

For California businesses, yes — particularly given commercial electricity rates that are nearly double the national average. Owned systems commonly achieve payback in 4–7 years, with systems designed to operate for 25+ years. The majority of a system's operational life generates electricity at effectively zero marginal cost.

Can I get commercial solar with no money down?

Yes. PPAs, solar leases, and C-PACE financing can all be structured with zero upfront payment. Each comes with different tradeoffs — PPAs and leases mean the third party claims tax incentives, while C-PACE preserves your ownership and ITC eligibility.

What is the federal Investment Tax Credit for commercial solar?

The ITC allows system owners to deduct 30% of total installation cost from federal income taxes. It applies to cash purchases, loan-financed ownership, and C-PACE (confirm with your tax advisor). Extended through at least 2032, it can also be combined with MACRS 5-year accelerated depreciation for additional savings.

What is C-PACE financing and is it available in California?

C-PACE lets commercial property owners repay solar costs through a voluntary property tax assessment rather than a traditional loan. California is an active C-PACE state with programs through administrators like WRCOG and LA County; qualification is based on property value rather than credit score, with terms up to 30 years.